I believe the way we traditionally think, and talk, about the broad-church of ‘ethical investing’ no longer serves us and needs a major update.

The core issue, is that we confuse and amalgamate two discrete, and equally important, strategies to achieve change:

- ESG integration + engagement (on the one hand)

- Impact, or investing in solutions (on the other)

We put them on an informal scale of ‘goodness’ and in the process, we do everyone (investors, society, the planet, and ourselves) a disservice.

This can have severe financial repercussions, as we discount the reality of impact-focussed companies tending to be the change-makers, which are likely to be growth focussed.

In a world of rising interest rates, these assets could be exposed to greater volatility.

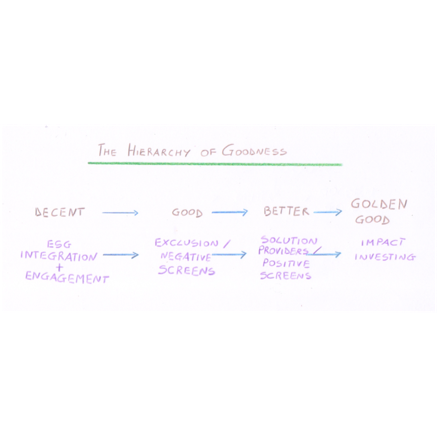

The Hierarchy of Goodness

By amalgamating investing in solutions and impact (let’s call it: “being good”) with ESG integration + engagement (let’s call it: “doing good”) and attaching value to investment strategies based on exclusion and empty promises that do not achieve change (let’s call it: “feeling good”), we create a de facto “hierarchy of goodness”.

One is “decent” if one integrates ESG in one’s investment process and engages with corporates;

One is “good” if you excludes the nasties;

“Better” if one only invests in solution providers;

And “Golden Good” if one goes for impact.

Beyond just defining terms, this hierarchy of goodness has investment style implications: While ESG integration is – barring a penchant for quality – style neutral, the more you move towards “Golden Goodness”, the more you move towards growth territory.

High-impact companies are solution seekers, they’re innovators proposing new ways forward, that they hope to scale.

Investing in them is inherently “growth investing”.

Growth Strategies Underperform in Rising Interest Rate Environments

We are at the start of a rising interest rate cycle. If we espouse this hierarchy of goodness, we need to tell investors that to move from mere decency to Golden Goodness, they need to swallow a period of underperformance, the length of which will be decided by the Fed.

Some – especially millennials, whose retirement is far, far away – will gladly swallow that underperformance.

Others – especially Gen Xs, whose retirement is near – can ill afford underperformance now; they will remember we told them they could have ‘Goodness’ without forgoing performance, and they’ll likely feel deceived, resent us, and possibly sack us.

Mandates are fickle things: winning them is hard work and keeping them requires:

- Good performance

- Trust

When you lose both, you’ll lose your mandates too.

Goodness Misconceptions

Between the two poles of doing good and being good, there is a bunch of stuff that makes us feel good but achieves little to no change.

Attaching value to it is a waste of everyone’s attention.

EXCLUSION DOES NOT CHANGE THE WORLD:

- Unless you manage hundreds AND hundreds of billions of dollars, exclusion strategies are not an effective tool for change. Why should anyone care that you are excluding? Why should any corporate leadership team listen to you?

- Exclusion is inherently conservative (I am right, you are wrong, we merrily go our separate ways and change nothing); it may make you feel pure, but it is not progressive. If you want change, get your hands dirty and engage.

DOMESTICALLY, EXCLUSION CAN – IN SOME CASES – JUST EQUATE TO VIRTUE SIGNALING:

Some ethical investors, especially the ones that have been in the market the longest approach exclusion with thoughtful care, they started there and opened the path for the rest of us and we owe them respect and gratitude.

For others, exclusion is a marketing tool that ticks the boxes of a questionnaire-based sector.

Let’s take Australia as an example:

- In Australia, excluding tobacco means excluding Amcor (and the supermarkets, if no revenue limit is in place or if that limit is set exceedingly low) excluding tobacco is a big statement with a small meaning

- Excluding cluster bombs and landmines means nothing: I don’t believe we have companies listed in Australia that make those nasty weapons, so if you manage Australian equity, bonds, infrastructure, or alternative assets, you can happily make this exclusion statement and go about your life without giving it another thought (or changing a single iota in the way you manage money)

- Ditto for pornography

- A similar argument can be made for signing up to the ‘alphabet soup’ of frameworks / principles / compacts / conventions / treaties /accords floating around, without backing that up with real work. It is possible: those are all voluntary groups, how much you contribute and how much joining means to you depends on how much you care: for some it is life-changing, for others it is just virtue-signalling. We score both with the same tick of the box.

For example, which Australian listed company knowingly employs children, or slave-labour?

- Doesn’t signing up to Human Rights conventions equate to a commitment to divesting if a scandal occurs? What change does that achieve?

- Isn’t the whole engagement work around modern slavery and supply chain transparency needed because as a society, we have turned a blind eye to modern slavery, we don’t know and must now push companies to meaningfully look?

Despite such shortfalls, many of us in ESG-land still parade these statements to communicate our goodness to investors. We talk that way and get scored by consultants and data providers on those metrics, and I’m increasingly convinced that we’re using a framework that no longer serves us.

So I ask…can we please collectively pause & reset?

A Way Forward

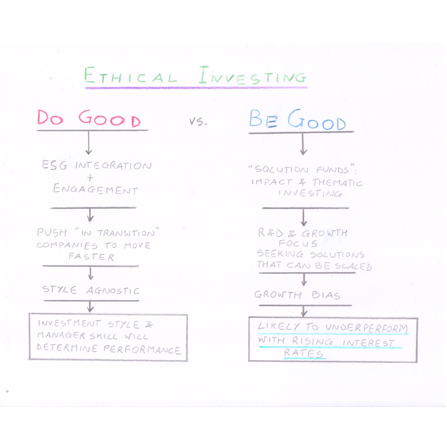

1) Let’s recognize that the hierarchy of goodness we are using no longer serves us, and, let’s unceremoniously ditch it

2) Let’s split our team and our investors into two groups:

- Do Good

- Be Good

3) Let’s go to work with renewed energy, with fit for purpose investment strategies, and with clear and honest communication:

- The “Do Good” team focuses on the bulk of the market: the incumbents, the “in transition”. Meaningfully research their strategies and powerfully engage with their leadership; cajole and push them to move faster towards best practice. And along the way, reduces portfolio risk.

- The “Be Good” team invests in the mavericks, the visionaries, the uncompromising change-makers. Support them with capital and guidance (good Governance & conservative gearing anyone?). Granted, the “Be Good” team will underperform initially, and will likely do so for as long as interest rates keep going up, but everyone understands that and there are no hard feelings.

4) Such proposed change has cost implications for asset consultants and data providers: questionnaire-based tick the box approaches will no longer work (did they ever?).

To assess process effectiveness, and evaluate whether the elusive-to-assess engagement work is done to a decent standard, expensive face-to-face time will need to be deployed.

Trust is central to this exercise, and that’s built on relationships, not questionnaires.

As in all models, the quality of outputs depends heavily on input quality: if we want a decent output that we can trust, we need to invest in quality inputs.

Yes: it is more expensive, and yes: it is worth it.

Maurizio Viani is an ESG consultant to the funds management industry. He works on the full range of ESG needs from strategy and investment process to research, policy documents and training manuals writing to stakeholder communication.

Maurizio’s key areas of interest are corporate engagement and the undeveloped opportunity that cooperation between corporates and NGOs represents. He has a long track record working in – predominantly qualitative – equity financial analysis both in Australia and overseas.